Home Construction Loan: A Complete Guide to Financing Your Dream Home

What Is a Home Construction Loan?

A home construction loan is a short-term, high-interest loan designed to finance the building of a new home. Unlike traditional mortgages, which cover the cost of an existing house, construction loans provide funds in stages as construction progresses. These loans typically have higher interest rates due to the increased risk for lenders but offer a practical way to fund custom-built homes.

How Home Construction Loans Work

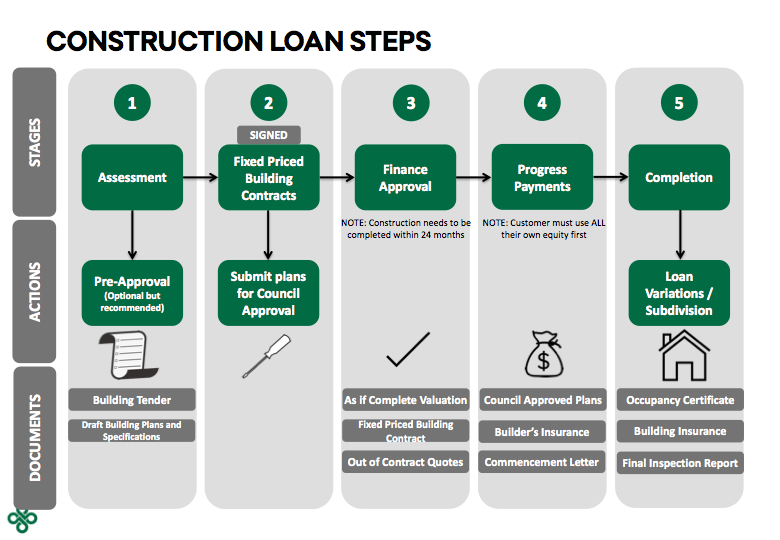

The process of obtaining and using a home construction loan involves several steps:

- Loan Approval: Borrowers must submit financial documents, a construction plan, and builder contracts.

- Fund Disbursement: Unlike a lump-sum mortgage, lenders release funds in stages (draw schedule) based on completed construction phases.

- Interest-Only Payments: Borrowers typically make interest-only payments during the construction phase.

- Loan Conversion: After construction is complete, some loans convert into a traditional mortgage.

Construction Loan vs. Traditional Mortgage

| Feature | Home Construction Loan | Traditional Mortgage |

|---|---|---|

| Loan Purpose | Funds new home construction | Buys an existing home |

| Disbursement | In stages based on project completion | Lump sum at closing |

| Interest Rates | Typically higher | Lower, fixed or variable |

| Payment Structure | Interest-only during construction | Regular principal & interest payments |

| Loan Duration | Short-term (6-18 months) | Long-term (15-30 years) |

Types of Home Construction Loans

Understanding the different types of home construction loans helps borrowers choose the best financing option.

Construction-to-Permanent Loan

- Converts into a traditional mortgage once construction is completed.

- Eliminates the need for separate loans and closing costs.

- Ideal for borrowers who plan to live in the home after construction.

Stand-Alone Construction Loan

- Covers only the construction phase.

- Requires a separate mortgage after completion.

- Suitable for those who expect to secure a better mortgage later.

Owner-Builder Construction Loan

- Allows borrowers to act as their own general contractor.

- Requires experience in home construction.

- Best for professionals in the building industry.

Renovation Loan

- Funds major home improvements or rebuilds.

- Can be used for remodeling an existing structure.

- Common options include FHA 203(k) loans and Fannie Mae HomeStyle loans.

Eligibility and Requirements for a Home Construction Loan

Lenders have strict criteria for approving construction loans to minimize risks.

Credit Score and Financial Stability

- Minimum credit score typically required: 620-680.

- Debt-to-income ratio should be below 45%.

- Proof of stable income and employment history.

Down Payment Requirements

- Higher than traditional mortgages, usually 20-25%.

- Some government-backed loans offer lower down payment options.

Construction Plan and Contractor Approval

- Lenders require a detailed blueprint and budget.

- Must work with a licensed and approved builder.

- Regular inspections to ensure work aligns with the plan.

Home Construction Loan Process: Step-by-Step

1. Prequalification and Loan Application

- Assess financial health and determine loan eligibility.

- Submit plans, cost estimates, and contractor details.

2. Loan Approval and Fund Disbursement

- Lenders review project feasibility and builder credentials.

- Funds are released in installments as each phase is completed.

3. Interest-Only Payments During Construction

- Monthly payments cover only the accrued interest.

- Principal repayment begins once construction is complete.

Pros and Cons of Home Construction Loans

Advantages of Construction Loans

- Customization: Allows homeowners to design and build their dream home.

- Controlled Funding: Funds are released in phases, ensuring accountability.

- Flexible Terms: Some loans convert into permanent mortgages.

Challenges and Risks

- Higher Interest Rates: More expensive than traditional home loans.

- Strict Approval Process: Requires detailed documentation and contractor verification.

- Potential Cost Overruns: If construction costs exceed the loan amount, borrowers must cover the difference.

Tips for Securing a Home Construction Loan

Improving Your Credit Score

- Pay off debts and reduce credit utilization.

- Check credit reports for errors and dispute inaccuracies.

Working with Reputable Builders

- Choose an experienced, licensed contractor with a solid reputation.

- Verify past projects and customer reviews.

Budgeting and Planning

- Get detailed cost estimates and include contingency funds.

- Monitor expenses to avoid cost overruns.

Alternatives to Home Construction Loans

If a construction loan isn’t the right fit, consider these alternatives:

Personal Loans and HELOCs

- Personal loans are unsecured and have higher interest rates.

- Home Equity Lines of Credit (HELOCs) use home equity as collateral.

Government-Backed Loans

- FHA Construction Loan: Lower down payment but stricter guidelines.

- VA Construction Loan: Available to eligible veterans with zero down payment options.

Table of Contents

Frequently Asked Questions (FAQ)

1. Can I use a construction loan to buy land?

Yes, some construction loans include land purchases, but eligibility depends on lender requirements.

2. What happens if construction costs exceed my loan amount?

Borrowers must cover additional costs or request a loan modification if eligible.

3. Do I need a separate mortgage after the construction loan?

It depends. Construction-to-permanent loans transition into a mortgage, while stand-alone construction loans require a separate mortgage.

4. What is a draw schedule?

A draw schedule outlines when loan funds are released based on project milestones.

5. Can I build a home with bad credit?

It’s challenging but possible with a higher down payment and lender approval.

6. Are construction loans interest-only?

Yes, most require interest-only payments during construction, with principal repayment starting afterward.

7. How long do construction loans last?

Most last 6-18 months, depending on the project timeline.

8. What if my construction project gets delayed?

Lenders may grant extensions, but additional costs and interest may apply.

Conclusion

A home construction loan is a powerful tool for financing a custom-built home. While they require careful planning, higher down payments, and detailed oversight, they provide flexibility and control over the home-building process. By understanding loan types, eligibility requirements, and the application process, borrowers can confidently secure financing for their dream home.